The best and worst case scenario for LNG prices

GAS INDUSTRY NEWS

Vijhay Krishnan (Rystad Energy)

3/16/2026

16 March 26 - Gas & LNG Market Analytics

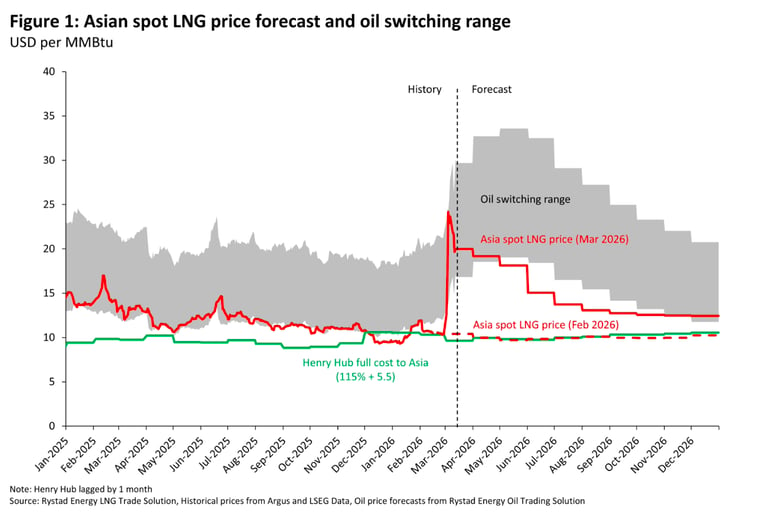

Rystad Energy has increased its 2026 Asian spot LNG prices to $14 per million British thermal units (MMBtu), an increase from $10 per MMBtu pre-conflict. This commentary will explain Rystad Energy’s view of spot liquefied natural gas (LNG) prices for 2026 as the Middle East conflict deepens and the Strait of Hormuz remains effectively closed. Rystad Energy’s base case assumes shipping traffic through the Strait is De Minimis through early April, with Qatari and UAE LNG production gradually fully restored by the second half of May.

2026 Asian spot LNG prices revised up to $14 per MMBtu

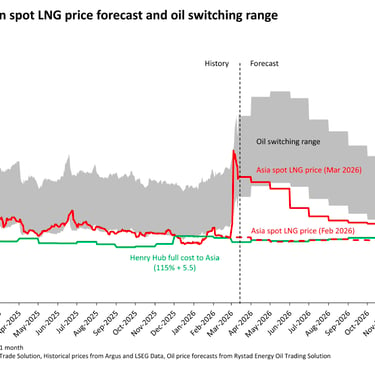

Our Asian spot prices have been revised up from $10 per MMBtu to $14 per MMBtu for 2026 (Figure 1). We have focused our forecast revision on Asian spot prices rather than the DutchTitle Transfer Facility (TTF) price, as the disruption to Middle Eastern LNG supply has shiftedprice-making power from Europe to Asia, where more than 85% of Qatar and UAE LNGproduction was received in 2025. This year, Europe will require an incremental 18 million tonnes (Mt) year on year, and therefore, TTF prices are determined by a no-arbitrage condition (the LNG shipping market remains structurally long in 2026) – $0.5 lower at $13.5 per MMBtu. These are yearly averages, and Figure 1 shows that monthly averages and daily/ intra-day figures could be much higher.

We observe the following:

Our pre-Iran war forecast implied that 2026 was a balanced year with spot prices close to the Long Run Marginal Cost (LRMC) of US LNG

As discussed before, the most exposed markets this time round are in South Asia, which fundamentally limits how high prices can go, compared to a disruption inenergy-security-focused Europe in 2022

Asian spot LNG prices briefly hit $25 per MMBtu but have since moderated to under $20per MMBtu, following the direction of oil prices

The current price environment will persist through the duration of the Strait of Hormuzclosure, but could increase if oil prices rise

Prices moderate as flows return to normal at the end of May, but retain a risk premiumrelative to the previous forecast. Delays to new start-ups such as Qatar’s North Field Expansion will also tighten 2027 balances

The situation is primarily a disruption to oil balances, and therefore LNG prices stay at the bottom end of the oil-products switching range and decouple once the situation returns to normal

LNG balances are not that bad… yet

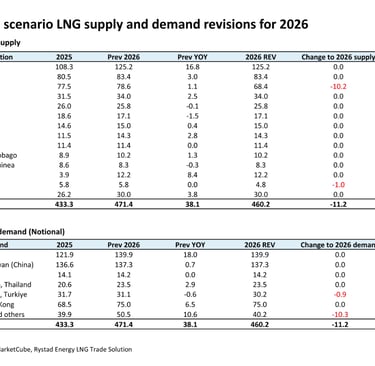

Supply:

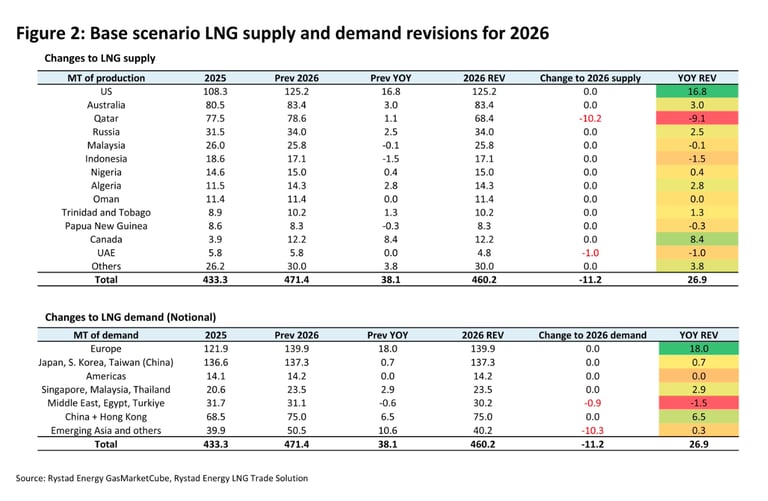

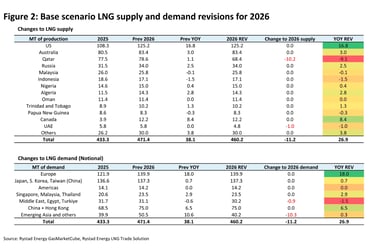

Pre-Iran war expectations for LNG supply additions were significant, with year-on-year growth of more than 30 Mt, driven by the US, Canada, and Australia

The loss of Qatari and UAE volumes for the duration of our base case is around 11 Mt, leaving over 25 Mt of LNG production growth on a net basis

This outlook assumes no disruption to Omani LNG, although this could still be at risk given that Iran has attacked Sohar, and some LNG offtakers are understood to be avoiding the region entirely

Demand:

Principal demand reduction is in emerging Asia. However, the base case scenario only requires the curtailment of LNG demand growth, rather than a reduction in 2025 demand figures, which moderates the impact

Close to 900,000 tonnes of Intra-Gulf LNG imports are impacted as Qatari LNG cannot flow to Kuwait, and external supply cannot pass the Strait of Hormuz

Note that the table in Figure 2 shows ‘notional’ demand outlooks, which are inputs to generate the price forecast. Actual LNG imports will adjust to the price forecast, and the demand reduction may be split across markets outside of emerging Asia that might have flexibility, such as through coal-fired power and demand-side management measures

A six-month disruption could see $30 per MMBtu in 2026

The $14 per MMBtu 2026 price forecast and previously explained 2026 revised balances follow a base case scenario of the Strait re-opening by early April

A more extreme scenario is possible – a six-month closure of the Strait as the conflict drags on, with full restoration assumed by September. This scenario may also eventuate from damage to LNG production facilities at Ras Laffan or Das Island

This would take approximately 40 Mt of LNG production off the market and would need curtailment even from price-inelastic demand in Europe and OECD Asia

TTF and Asian spot prices would follow oil higher to the vicinity of $30 per MMBtu for the year, as prices signal switching to heavy oil fuels. Still not as high as 2022, but close. These are yearly averages, and daily figures could be much higher

The market will remember

A potential disruption to the Strait of Hormuz has been discussed frequently over the past few years. The key surprise is the escalation in military action, with Iranian attacks on other Gulf nations, including Qatar, with whom they previously had cordial relations

‘Geostrategic’ sources of LNG supply that can reach their energy-security focused demand markets without travelling through chokepoints or current or potential disputed territory will fetch a reliability premium

It is in the long-term interest of the LNG Industry to see this conflict end as soon as possible and frame the situation as a ‘precautionary disruption’ with a quick return to normal rather than a prolonged outage in a conflict zone

The six-month disruption scenario could have a detrimental impact on long-term LNG demand in emerging markets, leading to even weaker prices in the early 2030s once the post-2022 wave of LNG projects is all online. Even energy security-focused markets may look at reworking their procurement plans to diversify away from the Middle East

Middle Eastern LNG players may re-double their efforts tto develop LNG supplies from other parts of the world, including APAC-facing supply

Source : Rystad Energy “The best- and worst-case scenario for LNG prices” Gas & LNG Market Analytics, 16 March 2026

16 March 26 - Gas & LNG Market Analytics

Rystad Energy has increased its 2026 Asian spot LNG prices to $14 per million British thermal units (MMBtu), an increase from $10 per MMBtu pre-conflict. This commentary will explain Rystad Energy’s view of spot liquefied natural gas (LNG) prices for 2026 as the Middle East conflict deepens and the Strait of Hormuz remains effectively closed. Rystad Energy’s base case assumes shipping traffic through the Strait is De Minimis through early April, with Qatari and UAE LNG production gradually fully restored by the second half of May.

2026 Asian spot LNG prices revised up to $14 per MMBtu

Our Asian spot prices have been revised up from $10 per MMBtu to $14 per MMBtu for 2026 (Figure 1). We have focused our forecast revision on Asian spot prices rather than the DutchTitle Transfer Facility (TTF) price, as the disruption to Middle Eastern LNG supply has shiftedprice-making power from Europe to Asia, where more than 85% of Qatar and UAE LNGproduction was received in 2025. This year, Europe will require an incremental 18 million tonnes (Mt) year on year, and therefore, TTF prices are determined by a no-arbitrage condition (the LNG shipping market remains structurally long in 2026) – $0.5 lower at $13.5 per MMBtu. These are yearly averages, and Figure 1 shows that monthly averages and daily/ intra-day figures could be much higher.

We observe the following:

Our pre-Iran war forecast implied that 2026 was a balanced year with spot prices close to the Long Run Marginal Cost (LRMC) of US LNG

As discussed before, the most exposed markets this time round are in South Asia, which fundamentally limits how high prices can go, compared to a disruption inenergy-security-focused Europe in 2022

Asian spot LNG prices briefly hit $25 per MMBtu but have since moderated to under $20per MMBtu, following the direction of oil prices

The current price environment will persist through the duration of the Strait of Hormuzclosure, but could increase if oil prices rise

Prices moderate as flows return to normal at the end of May, but retain a risk premiumrelative to the previous forecast. Delays to new start-ups such as Qatar’s North Field Expansion will also tighten 2027 balances

The situation is primarily a disruption to oil balances, and therefore LNG prices stay at the bottom end of the oil-products switching range and decouple once the situation returns to normal

LNG balances are not that bad… yet

Supply:

Pre-Iran war expectations for LNG supply additions were significant, with year-on-year growth of more than 30 Mt, driven by the US, Canada, and Australia

The loss of Qatari and UAE volumes for the duration of our base case is around 11 Mt, leaving over 25 Mt of LNG production growth on a net basis

This outlook assumes no disruption to Omani LNG, although this could still be at risk given that Iran has attacked Sohar, and some LNG offtakers are understood to be avoiding the region entirely

Demand:

Principal demand reduction is in emerging Asia. However, the base case scenario only requires the curtailment of LNG demand growth, rather than a reduction in 2025 demand figures, which moderates the impact

Close to 900,000 tonnes of Intra-Gulf LNG imports are impacted as Qatari LNG cannot flow to Kuwait, and external supply cannot pass the Strait of Hormuz

Note that the table in Figure 2 shows ‘notional’ demand outlooks, which are inputs to generate the price forecast. Actual LNG imports will adjust to the price forecast, and the demand reduction may be split across markets outside of emerging Asia that might have flexibility, such as through coal-fired power and demand-side management measures

A six-month disruption could see $30 per MMBtu in 2026

The $14 per MMBtu 2026 price forecast and previously explained 2026 revised balances follow a base case scenario of the Strait re-opening by early April

A more extreme scenario is possible – a six-month closure of the Strait as the conflict drags on, with full restoration assumed by September. This scenario may also eventuate from damage to LNG production facilities at Ras Laffan or Das Island

This would take approximately 40 Mt of LNG production off the market and would need curtailment even from price-inelastic demand in Europe and OECD Asia

TTF and Asian spot prices would follow oil higher to the vicinity of $30 per MMBtu for the year, as prices signal switching to heavy oil fuels. Still not as high as 2022, but close. These are yearly averages, and daily figures could be much higher

The market will remember

A potential disruption to the Strait of Hormuz has been discussed frequently over the past few years. The key surprise is the escalation in military action, with Iranian attacks on other Gulf nations, including Qatar, with whom they previously had cordial relations

‘Geostrategic’ sources of LNG supply that can reach their energy-security focused demand markets without travelling through chokepoints or current or potential disputed territory will fetch a reliability premium

It is in the long-term interest of the LNG Industry to see this conflict end as soon as possible and frame the situation as a ‘precautionary disruption’ with a quick return to normal rather than a prolonged outage in a conflict zone

The six-month disruption scenario could have a detrimental impact on long-term LNG demand in emerging markets, leading to even weaker prices in the early 2030s once the post-2022 wave of LNG projects is all online. Even energy security-focused markets may look at reworking their procurement plans to diversify away from the Middle East

Middle Eastern LNG players may re-double their efforts tto develop LNG supplies from other parts of the world, including APAC-facing supply

Source : Rystad Energy “The best- and worst-case scenario for LNG prices” Gas & LNG Market Analytics, 16 March 2026

Office:

Rasuna Office Park, 3rd Floor Unit TO-07

Complex Rasuna Epicentrum

Jl. HR. Rasuna Said, Kuningan, Jakarta 12960

Tel : +62 21 8378 3757, 8379 5203

Fax : +62 21 8378 1126, 8379 5302

Email : secretariat@indonesiangassociety.com

© 2014. Indonesian Gas Society. All rights reserved.

Mailing Address:

Jl.Kebon Baru 3 No.4 RT.03/RW.09 Tebet, Asem Baris,Jakarta Selatan, 12830